Public offices say a lot before anyone speaks. The floors, walls, and restrooms send signals the moment a visitor walks in. Tile plays a quiet but central role in that first impression. Clean, well-kept tile suggests order and care, often supported by regular tile cleaning routines that preserve both appearance and hygiene. Stained, cracked, or loose tile suggests the opposite and in a public setting, that difference matters. Tile is common in government buildings, municipal halls, courthouses, libraries, and service centers. It’s used because it’s durable, easy to clean, and moisture-resistant. But durable does not mean maintenance-free. Over time, grout darkens, surfaces dull, and chips appear. When that wear is ignored, it affects how people see the entire institution.

First Impressions Start at the Floor

When someone enters a public office, they notice the floor right away. Even if they don’t consciously think about it, they register its condition. Shiny, intact tile with clean grout feels orderly. It gives the sense that the space is well managed. On the other hand, stained grout, loose tiles, or visible cracks make a building feel neglected.

That perception extends beyond the floor itself. People tend to assume that visible conditions reflect invisible ones. If the lobby floor looks dirty, they may wonder about record keeping, processing times, or overall efficiency. It may not be fair, but it happens. Physical space influences trust.

Public offices handle sensitive tasks. They process permits, manage benefits, oversee public safety, and handle legal matters. Visitors often arrive stressed or uncertain. A clean, well-maintained space helps lower tension. It signals stability. Tile maintenance supports that quiet reassurance.

Hygiene and Public Confidence

Tile is common in restrooms, waiting areas, and service counters. These are high-touch, high-traffic zones. Grout lines absorb dirt and moisture. Without regular cleaning and sealing, they become dark and stained. In restrooms, this is especially noticeable.

People judge cleanliness quickly. Even minor discoloration can create doubt. If a restroom tile looks grimy, visitors may question the building’s overall sanitation standards. That doubt affects confidence in the institution itself.

Regular tile cleaning, grout sealing, and prompt repairs reduce these risks. They also protect health. Mold and mildew can grow in damp grout. Broken tiles can collect dirt and bacteria. In public settings with heavy use, preventive maintenance is not cosmetic. It’s practical.

Safety and Accessibility

Maintenance also affects safety. Cracked or uneven tiles create tripping hazards. Loose pieces can shift underfoot. In buildings that serve seniors, children, or people with disabilities, this risk increases.

Slip resistance matters as well. Polished tile can become slippery when wet. Proper cleaning methods and appropriate finishes help maintain traction. Replacing damaged sections quickly reduces liability and protects visitors.

Public offices are meant to be accessible. That includes physical safety. When tiles are level, intact, and properly maintained, the building feels reliable. People can focus on their purpose there, not on watching their step.

Cost Control and Long-Term Planning

Some offices delay tile maintenance to cut costs. On paper, this can look practical. But neglect often leads to higher expenses later. Small cracks spread. Water seeps under tiles. The adhesive weakens. Entire sections may need to be replaced rather than repaired.

Routine cleaning, sealing, and minor repairs extend the life of tile installations. They preserve the original investment. For public institutions that rely on taxpayer funds, responsible maintenance reflects responsible management.

Budget transparency matters in public settings. Visible deterioration can raise questions about how funds are used. Well-maintained facilities support the idea that resources are handled carefully. It’s a subtle message, but a powerful one.

Consistency Across Spaces

Public offices often include multiple rooms: lobbies, hallways, offices, meeting rooms, and restrooms. If some areas are spotless and others are clearly worn, the contrast stands out. Inconsistent maintenance suggests uneven priorities.

Tile condition should be consistent across the building. That does not mean every surface must look brand new. It means visible damage should be addressed, and

cleaning standards should remain steady. When visitors move from one area to another, the experience should feel coherent. Consistency builds credibility. It shows that attention to detail is not limited to public-facing areas only.

The Psychological Effect of Order

People respond to visual cues. Straight grout lines, aligned tiles, and smooth surfaces create a sense of structure. Disorder, even small visual breaks, can create subtle discomfort.

In public offices where decisions are made and documents are processed, order matters. The physical environment reinforces that expectation. Clean tile lines and intact surfaces mirror administrative clarity. They suggest that systems are in place and functioning.

This does not require luxury materials. Basic ceramic or porcelain tile can look professional when maintained properly. The key is care, not cost.

Staff Morale and Workplace Standards

The image of a public office affects employees, too. Staff members spend hours each day in these spaces. When floors and walls are clean and intact, the environment feels respected. That can influence morale.

Neglected surroundings can have the opposite effect. Employees may feel that standards are low or that their workplace is overlooked. Over time, that can shape behavior. People tend to rise or fall to the level of their environment.

Tile maintenance is part of a broader facility management strategy. It signals that the organization values its space and the people in it.

Practical Steps for Better Tile Maintenance

Public offices do not need elaborate renovation plans to improve their image. Small, steady actions make a difference:

- Schedule routine deep cleaning for tile and grout.

- Seal grout lines in high-moisture areas.

- Inspect floors regularly for cracks or loose tiles.

- Replace damaged sections promptly.

- Use cleaning products suited to the tile material.

These steps are not dramatic. But they prevent a gradual decline. And they maintain a baseline of professionalism.

A Reflection of Public Service

Public offices represent government, local administration, or community services. Their physical condition reflects public service standards. Tile may seem minor compared to policy or staffing. But it is one of the most visible elements in a building.

Visitors may forget the exact layout of a lobby. They may not remember the color of the walls. But they will remember whether the space felt clean and orderly.

Tile maintenance shapes that memory. It influences trust, comfort, and perception. And in public service, perception carries weight.

A well-maintained floor or restroom does not solve administrative challenges. But it enhances the institution’s credibility. It shows care in the details. And often, it’s the details people notice most.

Public offices say a lot before anyone speaks. The floors, walls, and restrooms send signals the moment a visitor walks in. Tile plays a quiet but central role in that first impression. Clean, well-kept tile suggests order and care, often supported by regular tile cleaning routines that preserve both appearance and hygiene. Stained, cracked, or loose tile suggests the opposite and in a public setting, that difference matters. Tile is common in government buildings, municipal halls, courthouses, libraries, and service centers. It’s used because it’s durable, easy to clean, and moisture-resistant. But durable does not mean maintenance-free. Over time, grout darkens, surfaces dull, and chips appear. When that wear is ignored, it affects how people see the entire institution.

Public offices say a lot before anyone speaks. The floors, walls, and restrooms send signals the moment a visitor walks in. Tile plays a quiet but central role in that first impression. Clean, well-kept tile suggests order and care, often supported by regular tile cleaning routines that preserve both appearance and hygiene. Stained, cracked, or loose tile suggests the opposite and in a public setting, that difference matters. Tile is common in government buildings, municipal halls, courthouses, libraries, and service centers. It’s used because it’s durable, easy to clean, and moisture-resistant. But durable does not mean maintenance-free. Over time, grout darkens, surfaces dull, and chips appear. When that wear is ignored, it affects how people see the entire institution.

Traditional Chinese women’s clothing is more than just fabric and design. It tells stories of power, identity, and politics. Over centuries, Chinese dress (source: robe chinoise) has reflected not just personal style but also rules set by the state. From emperors to revolutionaries, clothing has always played a role in shaping the image of women in society.

Traditional Chinese women’s clothing is more than just fabric and design. It tells stories of power, identity, and politics. Over centuries, Chinese dress (source: robe chinoise) has reflected not just personal style but also rules set by the state. From emperors to revolutionaries, clothing has always played a role in shaping the image of women in society.

Wall Street investment advisers and broker-dealer traders are being required to pay US regulators more than $470 million as fines for violating record keeping rules. In a statement made last Wednesday, officials of the US SEC and of the Commodity Futures Trading Commission (CFTC) that a number of entities providing broker-dealer and investment advice as a service, have violated the record-keeping rules; particularly, pertaining to communications about work-related matters

Wall Street investment advisers and broker-dealer traders are being required to pay US regulators more than $470 million as fines for violating record keeping rules. In a statement made last Wednesday, officials of the US SEC and of the Commodity Futures Trading Commission (CFTC) that a number of entities providing broker-dealer and investment advice as a service, have violated the record-keeping rules; particularly, pertaining to communications about work-related matters The main reason why SEC does not approve of using text, particularly WhatsApp messaging is that information conveyed by way of the application can be shared for securities trading purposes. The

The main reason why SEC does not approve of using text, particularly WhatsApp messaging is that information conveyed by way of the application can be shared for securities trading purposes. The  The overwhelming results of a new poll revealed that incumbent Prime Minister, Rishi Sunak will lose a majority of the parliamentary seats after the

The overwhelming results of a new poll revealed that incumbent Prime Minister, Rishi Sunak will lose a majority of the parliamentary seats after the  The results are actually considered surprising, shocking even, since the Labour Party just suffered a

The results are actually considered surprising, shocking even, since the Labour Party just suffered a

Clear and transparent communication is key.

Clear and transparent communication is key.

The UK parliament has a long record of lobbying scandals, as influential people paid lobby groups to exert efforts in influencing legislations in their favour. However, there seems to be no end in sight for the series of lobbying scandals that frequently rock the UK parliament. The situation leaves many British entrepreneurs apprehensive over potential laws that could negatively affect their

The UK parliament has a long record of lobbying scandals, as influential people paid lobby groups to exert efforts in influencing legislations in their favour. However, there seems to be no end in sight for the series of lobbying scandals that frequently rock the UK parliament. The situation leaves many British entrepreneurs apprehensive over potential laws that could negatively affect their  Despite the scandals and the subsequent resignations of the MPs involved, the lobbying industry has been rapidly flourishing since the 1990s. While it was estimated in 2007 that the industry was worth £1.9 billion, new 2022 released in data indicates that the interest groups APPG received as much as GBP13 million from private firms; apparently satisfied with the results of lobbying activities during the year.

Despite the scandals and the subsequent resignations of the MPs involved, the lobbying industry has been rapidly flourishing since the 1990s. While it was estimated in 2007 that the industry was worth £1.9 billion, new 2022 released in data indicates that the interest groups APPG received as much as GBP13 million from private firms; apparently satisfied with the results of lobbying activities during the year.

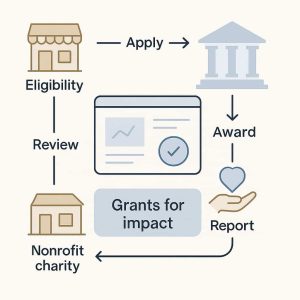

Government grants can be a lifeline for small businesses and charities, funding projects that might otherwise remain ideas on paper. Grants support equipment upgrades, community programs, research initiatives, facility improvements, and public education work, but they are not as simple as applying and waiting for a check to arrive. They follow defined structures, serve very specific funding goals, and come with compliance requirements, reporting rules, and restrictions on how the money can be used. These rules can surprise first-time applicants who expect fast approval or total spending freedom. Understanding the system early helps organizations evaluate fit, prepare properly, and avoid costly missteps. Many small nonprofits turn to guides to build that clarity, including Stand With Main Street resources, which break down business-focused resources to help founders and charity leaders navigate grants and formation decisions with more confidence and less wasted time.

Government grants can be a lifeline for small businesses and charities, funding projects that might otherwise remain ideas on paper. Grants support equipment upgrades, community programs, research initiatives, facility improvements, and public education work, but they are not as simple as applying and waiting for a check to arrive. They follow defined structures, serve very specific funding goals, and come with compliance requirements, reporting rules, and restrictions on how the money can be used. These rules can surprise first-time applicants who expect fast approval or total spending freedom. Understanding the system early helps organizations evaluate fit, prepare properly, and avoid costly missteps. Many small nonprofits turn to guides to build that clarity, including Stand With Main Street resources, which break down business-focused resources to help founders and charity leaders navigate grants and formation decisions with more confidence and less wasted time.

Cities, at their core, are communities where people live, work, and strive to thrive. But in the rush of modern urban life, wellness often takes a back seat. From chronic stress and mental health challenges to limited access to quality care, city residents face mounting obstacles. That’s why local governments are increasingly being called upon—not just

Cities, at their core, are communities where people live, work, and strive to thrive. But in the rush of modern urban life, wellness often takes a back seat. From chronic stress and mental health challenges to limited access to quality care, city residents face mounting obstacles. That’s why local governments are increasingly being called upon—not just

Storytelling is one of the most powerful tools in shaping political opinions and influencing public discourse. Videos have become the go-to medium for delivering impactful political messages, whether for campaigns, activism, or issue awareness. Wondershare Filmora, known for its simplicity and creative capabilities, has emerged as a valuable resource for those wanting to craft compelling narratives in the political arena.

Storytelling is one of the most powerful tools in shaping political opinions and influencing public discourse. Videos have become the go-to medium for delivering impactful political messages, whether for campaigns, activism, or issue awareness. Wondershare Filmora, known for its simplicity and creative capabilities, has emerged as a valuable resource for those wanting to craft compelling narratives in the political arena.

Many rubbish removal companies offer different pricing structures, such as flat rates or fees based on weight. It’s crucial to do your research and compare options available in your area. Some services might provide inclusive packages, covering everything from pick-up to disposal, while others may charge extra for additional services like sorting or recycling. Understanding these distinctions can help you make a more informed decision that aligns with your budget and needs.

Many rubbish removal companies offer different pricing structures, such as flat rates or fees based on weight. It’s crucial to do your research and compare options available in your area. Some services might provide inclusive packages, covering everything from pick-up to disposal, while others may charge extra for additional services like sorting or recycling. Understanding these distinctions can help you make a more informed decision that aligns with your budget and needs. Once you have narrowed down your options, inquire about the range of services they offer. A rubbish removal Glasgow company provides comprehensive solutions that include not only the collection and disposal of waste but also additional services like recycling and hazardous waste management. It’s important to find a service that matches your specific requirements, especially if you have different types of rubbish that need to be handled differently. Additionally, check if the company offers same-day services or flexible scheduling, as this can be particularly beneficial during urgent cleanouts.

Once you have narrowed down your options, inquire about the range of services they offer. A rubbish removal Glasgow company provides comprehensive solutions that include not only the collection and disposal of waste but also additional services like recycling and hazardous waste management. It’s important to find a service that matches your specific requirements, especially if you have different types of rubbish that need to be handled differently. Additionally, check if the company offers same-day services or flexible scheduling, as this can be particularly beneficial during urgent cleanouts. At first glance, politics and wash-and-fold laundry services might seem unrelated. However, the influence of local government regulations and policies can significantly affect the operations of small businesses, including Seattle wa wash and fold laundry service. From minimum wage laws to environmental regulations, politics often has a direct impact on how these businesses function and serve their communities.

At first glance, politics and wash-and-fold laundry services might seem unrelated. However, the influence of local government regulations and policies can significantly affect the operations of small businesses, including Seattle wa wash and fold laundry service. From minimum wage laws to environmental regulations, politics often has a direct impact on how these businesses function and serve their communities.

In recent years, a connection has emerged between politics and the vintage trailer modernization. This may seem an odd combination, but as with many things in today’s world, the connection is both intriguing and complex. On one hand, politics shape the regulatory environment and incentives for such modernization. On the other, the revival of vintage trailers speaks to a broader societal trend towards sustainability and nostalgia.

In recent years, a connection has emerged between politics and the vintage trailer modernization. This may seem an odd combination, but as with many things in today’s world, the connection is both intriguing and complex. On one hand, politics shape the regulatory environment and incentives for such modernization. On the other, the revival of vintage trailers speaks to a broader societal trend towards sustainability and nostalgia.

Going here on weekends at early hours of the busiest day is highly recommendable especially for those who want to escape the crowds. Weekend evenings is also a good time to pick when you like to go here.

Going here on weekends at early hours of the busiest day is highly recommendable especially for those who want to escape the crowds. Weekend evenings is also a good time to pick when you like to go here. Understanding political responsibilities can feel like staring at an unscratched lottery ticket. You know there’s something important underneath, not just the duty to “Unscratchthesurface”. This analogy isn’t just fancy talk; it’s a simple way to dive into how political duties are much more than what meets the eye.

Understanding political responsibilities can feel like staring at an unscratched lottery ticket. You know there’s something important underneath, not just the duty to “Unscratchthesurface”. This analogy isn’t just fancy talk; it’s a simple way to dive into how political duties are much more than what meets the eye.